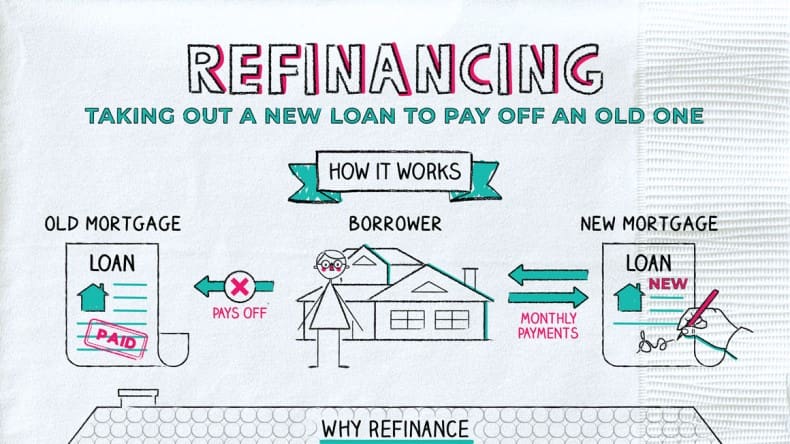

There are many reasons why you might want to consider refinancing your mortgage. Perhaps you are unhappy with your current interest rate, or you would like to shorten the term of your mortgage. Maybe you want to eliminate mortgage insurance or consolidate high-interest rate debt. There are many reasons to refinance, and in this blog post, we will explore seven of them! So, if you are thinking about refinancing your mortgage, read on!

To Obtain a Lower Interest Rate

One of the most common reasons people refinance their mortgage is to obtain a lower interest rate. If interest rates have dropped since you originally obtained your mortgage, you may be able to save money by refinancing. Even a small reduction in your interest rate can add up to big savings over the life of your loan! However, it is important to know every single piece of information on refinancing since it can be different for each person. You should also be aware of the fees associated with refinancing, which can include things like appraisal fees, title insurance, and origination charges. By knowing all of this information, you can make an informed decision about whether or not refinancing is right for you

To Shorten the Term of the Mortgage

Another popular reason to refinance is to shorten the term of the mortgage. By refinancing from a 30-year loan to a 15-year loan, for example, you can save a lot of money in interest over the life of the loan. You will also build equity in your home much faster with a shorter loan term. Of course, your monthly payments will be higher with a shorter loan term, so you need to make sure you can afford the new payment before you refinance. In addition, remember that you may have to pay fees to refinance, so be sure to factor those into your decision.

Eliminate Mortgage Insurance

If you obtained your mortgage through the Federal Housing Administration (FHA), you are required to pay mortgage insurance. This insurance protects the lender in case you default on your loan. However, once you have paid off a certain amount of your loan, you may be eligible to cancel the mortgage insurance. This can save you a significant amount of money each month, and it may make refinancing worthwhile. Be sure to talk to your lender about this before you refinance, as there are specific requirements that must be met. These requirements can include things like having a good payment history and having a certain amount of equity in your home.

Consolidate High-Interest Rate Debt

If you have high-interest rate debt, such as credit card debt, you may be able to save money by consolidating that debt into your mortgage. When you do this, you can take advantage of the lower interest rate on your mortgage and pay off your debt more quickly. This can be a great way to get rid of high-interest debt and save money at the same time! However, you need to be careful not to increase the amount of debt you have by consolidating. You also need to make sure you can afford the new monthly payment on your mortgage. To do so, be sure to include the additional debt in your monthly budget before you refinance. In addition, remember that you will likely have to pay fees to refinance, so factor those into your decision as well.

Rise Your Home’s Equity

Over time, as you make payments on your mortgage, you will build equity in your home. This equity can be used for things like home improvements, investments, or even college tuition. If you have built up a significant amount of equity in your home, you may be able to use it to rise by refinancing. When you do this, you take out a new loan for more than you owe on your current mortgage. The difference between the two loans is given to you in cash, which you can use however you like. Of course, this option should be used carefully, as it can put your home at risk if you default on the loan. Be sure to talk to a financial advisor before you decide to refinance for this reason. In addition, also keep in mind that you will have to pay fees to refinance, so factor those into your decision.

Buy-Out Your Ex-Spouse

If you are going through a divorce, you may be able to use refinancing to buy out your ex-spouse’s interest in the home. This can be a great way to keep the home in your name and avoid having to sell it. In order to do this, you will need to refinance the mortgage for more than you currently owe. The difference between the two loans will be given to your ex-spouse in cash. Of course, this option should be used carefully, as it can put your home at risk if you default on the loan. Be sure to talk to a financial advisor before you decide to refinance for this reason. In addition, also keep in mind that you will have to pay fees to refinance, so factor those into your decision.

Obtain Some Extra Cash

In some cases, you may be able to refinance your mortgage for more than you currently owe and take the difference in cash. This cash can be used however you like, but it is important to remember that this option puts your home at risk if you default on the loan. When deciding whether or not to refinance for cash, be sure to consider your goals and create a budget to ensure you will be able to make the payments.

If you are struggling with high-interest rates or monthly mortgage payments, refinancing may be a good option for you. These seven reasons are just some of the many benefits that come with refinancing your mortgage. Be sure to talk to your lender about this before you refinance, as there are specific requirements that must be met. These requirements can include things like having a good payment history and having a certain amount of equity in your home. By doing your research and talking to your lender, you can be sure that refinancing is the right choice for you.